Buying a Strip Mall in California: What the Numbers Look Like Before You Make an Offer

June 21, 2026

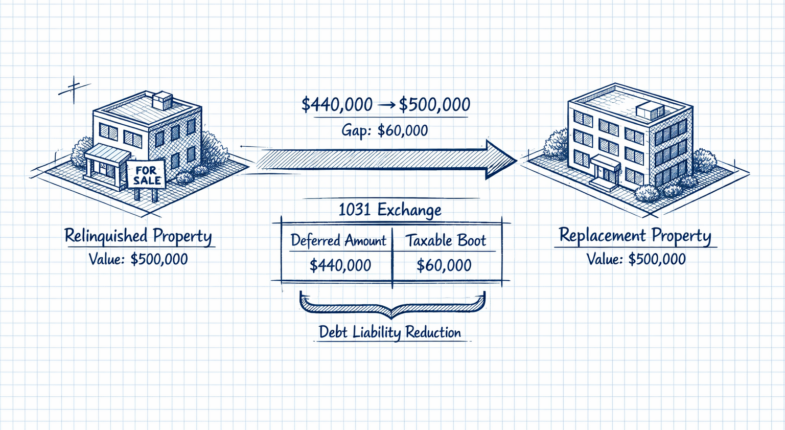

1031 Exchange Mistakes That Cost San Diego Investors: Boot, Timelines, and Identification Errors

June 23, 2026

Heading into 2026, the San Diego industrial market is sitting at a 9.6% vacancy rate - a meaningful reset from the sub-4% readings that defined the pandemic boom - while asking rents have settled around $1.46 per square foot NNN. On the investment side, $260 million in industrial sales closed in Q1 2026 alone, and it tells that capital hasn’t walked away - it’s recalibrating. The buyers active are working with different underwriting assumptions, different return expectations and a sharper eye on submarket fundamentals than the wave of investors who piled in four years ago.

That difference between the frenzy and the present is where the story lives. San Diego’s industrial base is not monolithic - Otay Mesa, Miramar, Kearny Mesa and Sorrento Valley are each behaving differently, absorbing new supply at different rates and attracting different tenant profiles. Rents haven’t collapsed. But they haven’t kept climbing either. Lease structures are changing. And the supply-side pressures that kept this market so constrained for so long haven’t disappeared - they’ve just changed shape.

This piece breaks down where vacancy actually stands across San Diego’s core industrial submarkets, what tenants are paying and agreeing to in today’s leases and what investors buying industrial assets are watching closely that their 2021 counterparts largely ignored.

Key Takeaways

- San Diego’s industrial vacancy hit 9.6% with asking rents at $1.46/sf NNN, down 3.7% year-over-year.

- Submarkets behave differently: Otay Mesa faces oversupply pressure while Miramar and Kearny Mesa stay tighter due to land constraints.

- Landlords now offer free rent and tenant improvement allowances more frequently, unlike the landlord-favored conditions of 2022.

- Demand is diversified across defense, cross-border manufacturing, life sciences, and last-mile delivery, reducing single-sector dependency.

- Land scarcity and slow entitlements structurally limit new supply, capping how far vacancy can rise long-term.

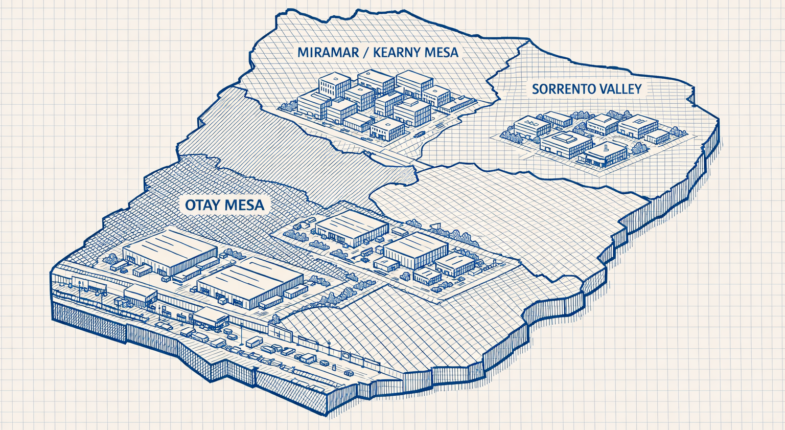

Vacancy by Submarket: How Otay Mesa, Miramar, Kearny Mesa, and Sorrento Valley Compare

San Diego’s industrial vacancy sits at 9.6%, with total availability climbing to 13.0%, reflecting spaces being marketed but not yet empty. Those numbers tell part of the story. But the picture only comes clear when you look at each submarket on its own terms.

Otay Mesa is the one to watch for logistics. Its proximity to the US-Mexico border makes it a natural home for cross-border distribution and manufacturing-adjacent operations. Vacancy there has loosened compared to the frenzy of 2021 and 2022, partly because a wave of new supply got delivered into a market where demand had already started to cool. Landlords in Otay Mesa are feeling that pressure more directly than their counterparts elsewhere in the county.

Miramar and Kearny Mesa work a bit differently. These submarkets pull in a wider combination of tenants - light industrial users, contractors, and smaller distribution outfits that want ready access to the metro area. Because the land base is more constrained and new construction is harder to pencil in, vacancy stays tighter. Tenants who want functional, mid-size industrial space in a central location find demand reasonably steady here. Learn more about commercial property management in Miramar and how owners navigate this market.

Sorrento Valley is its own category - it attracts life sciences and biotech-adjacent users who blur the line between traditional industrial and lab space. That tenant profile means the submarket responds to different economic signals than a pure logistics corridor would. Defense-related users also have a footprint nearby, which can add some stability to demand. See how Sorrento Valley property management differs from other parts of the county.

The difference between vacancy and availability across all four submarkets is worth mentioning. A landlord sitting on vacant space in Otay Mesa is in a different position than one working to reduce vacancy in Sorrento Valley to biotech tenants who plan twelve to eighteen months out. Same county, very different process.

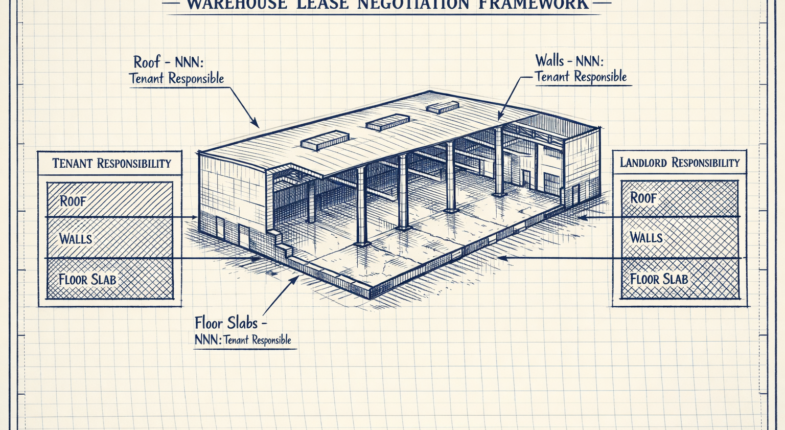

Asking Rents and Lease Structures Shaping Today’s Deals

The average asking rent across San Diego’s industrial market sits at $1.46 per square foot on a NNN basis, which is down about 3.7% from a year ago. That drop is modest in percentage terms. But it tells something actual: landlords are no longer holding the line the way they were in 2022 and 2023.

A NNN lease means the tenant pays base rent, their share of property taxes, insurance, and maintenance costs. For industrial users, this is the standard structure - it puts more of the operating cost responsibility on the tenant, so the $1.46 figure is the starting point of what a tenant will pay each month.

What’s changed more noticeably is how landlords are sweetening deals to get leases signed. Free rent periods and tenant improvement allowances are showing up with frequency now, and tenants who push for these concessions are usually getting them. In 2022, a landlord could fill a space with the first tenant who showed up - it’s not that environment right now.

Gross leases, where the landlord covers operating costs, are still rare in the industrial world. But they do appear in some smaller or older multi-tenant buildings where the landlord prefers to control costs - it’s worth asking about if you’re looking at legacy product in submarkets like Kearny Mesa.

The helpful takeaway for tenants negotiating a lease is that the conversation is more open than it was two years ago. You can reasonably ask for a few months of free rent at the start of a term, push for an actual TI allowance to fit out the space, and negotiate rent escalation caps into a longer-term deal. None of those asks would have gone far in the tighter market of 2022.

Rates also vary across submarkets, so the $1.46 average doesn’t tell the full story on its own - which is worth keeping in mind as we get into what’s actually pulling tenants into the market.

What’s Actually Driving Industrial Demand in San Diego Right Now

San Diego’s industrial tenants don’t look like those you’d find in the Inland Empire or Los Angeles. The market here runs on a combination of industries tied closely to the region’s geography and economic identity.

Defense contractors and aerospace suppliers take up a actual share of leased space. San Diego’s concentration of military installations and defense-related employers creates steady demand for functional industrial buildings - not flashy, just reliable and well-located. That tenant tends to sign longer leases and stay put.

Cross-border manufacturing is another driver. A lot of businesses run split operations between San Diego and Tijuana, and they need warehouse or light industrial space on the U.S. side to manage logistics, compliance, and final assembly - something the Inland Empire basically can’t replicate. Proximity to the border is part of the product.

Life sciences has also pushed into industrial. Lab and research space is expensive and hard to find, so some tenants spill into industrial buildings that can support their needs - it’s not the dominant story. But it’s a visible one in submarkets near biotech corridors.

E-commerce fulfillment and cold storage round out the picture. Population density along the coast makes last-mile delivery space valuable, and demand for temperature-controlled buildings has grown with food and pharmaceutical distribution needs. These users tend to prioritize location over building style.

The 2.1 million square feet of leasing volume recorded in Q1 across 348 transactions reflects this diversity. The deal count matters as much as the square footage - it tells you the market isn’t being carried by a handful of large tenants but by a large base of mid-size users across multiple industries.

That breadth is what separates San Diego from markets that depend heavily on big-box logistics. Demand here is fragmented in a healthy way, spread across tenant types that aren’t all responding to the same economic pressures at once. Managing industrial properties in San Diego means understanding this mix and positioning assets to serve it effectively.

Buying Industrial in San Diego Today vs. the 2021-2022 Peak

The numbers look different. San Diego industrial assets are trading at around $307 per square foot and Q1 2025 saw roughly $260 million in total sales volume; it’s still an active market. But the conditions behind those numbers are nothing like what drove deals two and three years ago.

At the 2021-2022 peak, cap rates compressed hard and buyers were waiving contingencies to win deals. Financing was cheap, tenant demand felt unlimited and investors built their underwriting around rent growth assumptions that turned out to be unsustainably optimistic. Due diligence got lighter. The logic was that even a flawed deal would fix itself if the market kept moving the way it was moving.

That logic doesn’t hold the same way today. Debt costs are higher, so the math on acquisitions has to be tighter from the start. Buyers are spending more time on lease rollover risk, tenant credit quality and how much vacancy exposure they can absorb if a tenant exits. These were not ignored at the peak, but they were treated as minor concerns in a fast-moving market.

CBRE’s negative 554,857 square foot net absorption reading for San Diego adds weight to that scrutiny. Negative absorption doesn’t mean the market is broken. But it does mean more space is being vacated than occupied and that changes how you model near-term income stability on any given asset.

Financing assumptions are also under a microscope. Buyers in 2021 and 2022 could use favorable loan terms to make deals work even with thin going-in yields. That cushion is gone. Investors are underwriting more conservatively and expecting longer hold periods to hit their return targets.

The deals still get done and San Diego’s fundamentals give buyers reasons to stay involved. But the tolerance for loose underwriting has narrowed considerably since the peak.

Land Scarcity, Entitlements, and the Supply Ceiling Keeping Availability in Check

San Diego’s industrial market has long faced a fundamental constraint: flat, buildable land is effectively gone. It’s not a new problem, but it’s one that becomes more relevant as investors try to figure out how much vacancy can climb before the market self-corrects.

The entitlement process in California is legitimately slow. Environmental review alone can add years to a project timeline, and that’s before you factor in infrastructure requirements, community input periods, and agency coordination. A developer who wants to break ground on a new industrial building in San Diego is competing for land and against time.

Residential and mixed-use conversion pressure makes this even tighter. Parcels that may have been industrial candidates five years ago are now in play for housing, which local governments prioritize. That pulls possible industrial land out of the pipeline before it gets a chance to be developed for warehousing or flex use. Rezoning commercial property to residential in San Diego has become an increasingly common path for landowners navigating this shift.

In practice, new supply has a structural ceiling. Even in a softer market, the overbuilding that has pushed vacancy into double digits in some Sun Belt metros is unlikely here. CoStar projects that national industrial vacancy will peak around 7.8% before declining through 2027, and San Diego’s constraints suggest its own cycle could be comparatively shorter.

For investors willing to hold through the latest soft patch, this matters. The same friction that makes San Diego hard to build in also makes it hard to flood with new product. Vacancy at 9.6% is elevated, but the structural limits on new deliveries put a natural boundary on how far that number can run.

That’s the underlying logic for investors who are still paying attention to San Diego’s industrial market even amid the near-term softness. The supply side of the equation is working in their favor, even when the demand side is quiet.

What the Data Is Telling Investors Who Are Paying Attention

The next 12 to 18 months will probably reward those who underwrite instead of chasing momentum or waiting for capitulation. Expect continued pressure on older, functionally obsolete product while well-located Class A assets with modern heights and power capacity hold their ground on rents. The Otay Mesa and Chula Vista submarkets bear close watching as border trade volumes and nearshoring activity continue to evolve - any actual change there will move through industrial demand faster than most metrics will capture in time.

The helpful step is simple: get granular. Market-level data will only tell you so much in a region where submarket pace and deal-level fundamentals diverge. If you are looking at an asset or a position in San Diego industrial, the questions worth pressing are about lease rollover exposure, replacement cost relative to asking price, and what the tenant base actually does for a living. Those answers will matter more over the next cycle than any single forecast about where vacancy lands by year-end. A commercial property manager familiar with these submarkets can help you stress-test those assumptions before you commit.

FAQs

What is San Diego's current industrial vacancy rate?

San Diego's industrial vacancy rate sits at 9.6% heading into 2026, with total availability at 13.0%. This is a significant increase from the sub-4% rates seen during the pandemic boom.

What are current industrial asking rents in San Diego?

Asking rents average $1.46 per square foot NNN, down 3.7% year-over-year. Landlords are increasingly offering free rent periods and tenant improvement allowances to secure leases.

Which San Diego industrial submarket has the most vacancy pressure?

Otay Mesa faces the most vacancy pressure due to new supply being delivered as demand cooled. Miramar and Kearny Mesa remain tighter because land constraints limit new construction.

What industries drive San Diego's industrial demand?

Demand comes from defense contractors, cross-border manufacturing, life sciences, and last-mile delivery. This diversity across sectors reduces dependency on any single industry, making the market more resilient.

Why can't San Diego's industrial vacancy rise indefinitely?

Scarce buildable land, slow California entitlement processes, and residential rezoning pressure create a structural ceiling on new supply, naturally limiting how high vacancy can climb long-term.