How Commercial Properties Are Valued in California: Cap Rate, GRM, and What Sellers Often Miss

June 20, 2026

San Diego’s Industrial Market in 2026: Vacancy, Rents, and What Investors Are Watching

June 22, 2026

The challenge with buying retail real estate is that the numbers on a broker’s offering memorandum are rarely the whole story. A stabilized center with a national anchor looks very different from a half-vacant strip with a dark grocery store and a lease full of co-tenancy clauses - but might carry a similar asking cap rate on paper. The difference between a sound acquisition and an expensive lesson usually depends on how closely you interrogate the deal before you buy - not after.

This is written for buyers who are past the introductory stage. You already understand net operating income and you’re not here for a glossary. What you need is a picture of how cap rates actually vary across San Diego’s submarkets, what a strong anchor tenant does to valuation and risk profile, which due diligence flags are too easy to miss, and how to model a basic value-add scenario so you can walk into negotiations with confidence - and that’s what this breaks down.

Key Takeaways

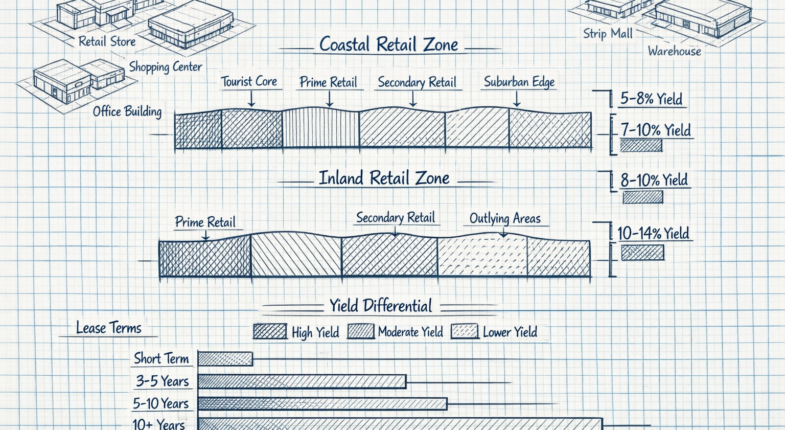

- San Diego strip mall cap rates range 5.0%-6.5%, with coastal submarkets compressing lower and inland areas offering higher but riskier yields.

- Anchor tenants improve financing terms and NOI predictability, but co-tenancy clauses can trigger rent cuts or early terminations if anchors go dark.

- Due diligence must include reviewing co-tenancy clauses, deferred maintenance, and unresolved CAM disputes-items not visible on a standard rent roll.

- Value-add underwriting requires modeling current NOI, stabilized NOI, and all capital costs before assuming vacant space represents genuine upside.

- Buying at a higher cap rate and stabilizing to a lower one can generate returns beyond NOI growth alone through cap rate compression.

What Cap Rates Actually Look Like Across San Diego Submarkets Right Now

CBRE’s Q1 2026 data puts the national average cap rate at 6.44% for small strip centers and 6.55% for bigger neighborhood centers. San Diego runs a bit below that, with most deals landing somewhere in the 5.0% to 6.5% range depending on the asset and its location.

That range is wide enough to matter. A deal at 5.2% and a deal at 6.4% can look similar on paper but feel very different once you run the cash flow numbers.

Location does the work here. Coastal submarkets like La Jolla, Del Mar, and Encinitas compress toward the lower end of that band because demand for retail space there stays strong and vacancy rates stay low. Buyers accept less yield in exchange for more stability and the expectation that rents will hold up over time.

Inland submarkets show something different. Areas like El Cajon, Santee, and Lakeside trade closer to the 6.0% to 6.5% range. That extra yield comes with higher vacancy danger and a tenant pool that’s more sensitive to economic pressure. The yield is higher because the asset carries more uncertainty.

Beyond geography, a few other things push a deal up or down within that band. Lease term length is a big one. A center where most tenants have three or fewer years left on their leases will price at a higher cap rate than one with long-term leases locked in. Tenant credit quality matters too, and so does the condition of the physical asset. Deferred maintenance gives buyers reason to push the cap rate up because they are pricing in future costs.

Rent-to-market is another factor worth mentioning. If existing rents are below what comparable spaces are leasing for, that can work in a buyer’s favor - but sellers know this too and will argue for a lower cap rate based on upside potential. That is a negotiation, not a fixed rule.

The submarket sets a rough ceiling and floor, and everything about the asset moves the number within that window. Location tells you where to start; the lease structure and building condition tell you where to land.

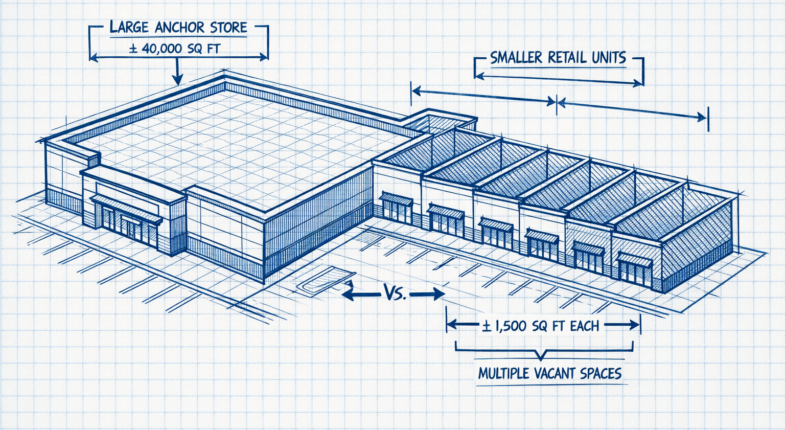

How an Anchor Tenant Shifts the Valuation Math on a Strip Center

An anchor tenant - think a grocery store, pharmacy, or national credit retailer - does more than fill square footage; it changes how a lender reads the deal and how a buyer should price the income stream.

Lenders treat anchored centers differently because the NOI is more predictable. A Kroger or CVS on a long-term lease with scheduled rent bumps gives a lender confidence, and that confidence translates into better loan terms. You can sometimes access lower interest rates and higher loan-to-value ratios on an anchored center than you would on a multi-tenant strip with smaller local retailers.

That stability also changes your underwriting assumptions. When you model out an anchored center, you’re working with a more reliable income floor. The anchor’s lease term sets a baseline that the rest of the pro forma builds around; it’s worth something in the valuation, and buyers and brokers will price it in accordingly - which is why anchored centers trade at compressed cap rates compared to unanchored ones.

That anchor dependency cuts both ways.

When an anchor goes dark - meaning it vacates before the lease ends or lets the lease expire - the effect on co-tenants can be fast and severe. Smaller tenants in a strip center frequently rely on the traffic an anchor pulls in. If that foot traffic disappears, their own sales drop, and some will look to exit co-tenancy clauses in their leases. Those clauses can allow co-tenants to cut back on rent or terminate early if the anchor leaves; it’s a scenario worth modeling before signing - not after.

West Coast strip centers are running occupancy rates around 95% to 96% right now, which looks healthy on the surface. But high occupancy makes it harder to see anchor dependency in the numbers. A center that’s nearly full still has a concentration problem if one tenant accounts for 40% or more of the gross leasable area.

The helpful takeaway for valuation is to look at what the NOI looks like with the anchor removed from the picture. If the math falls apart without them, the price needs to reflect that exposure - and you’ll need to know what the lease terms say about what happens if they leave.

Strip Mall Acquisition Due Diligence: The Retail-Specific Red Flags That Kill Deals

Retail leases carry terms that you won’t find in office or industrial deals, and some of them can quietly change the income picture after you close. Co-tenancy clauses are the biggest example. These are provisions that give a tenant the right to cut back on their rent or terminate their lease early if a named anchor tenant leaves or if occupancy drops below a set threshold.

This matters quite a bit if you’re buying a center where one large tenant drives foot traffic for everyone else. A co-tenancy clause buried in a junior tenant’s lease can turn a stable rent roll into a moving target the second that anchor goes dark. Pull every lease and read these sections before you get emotionally attached to the numbers.

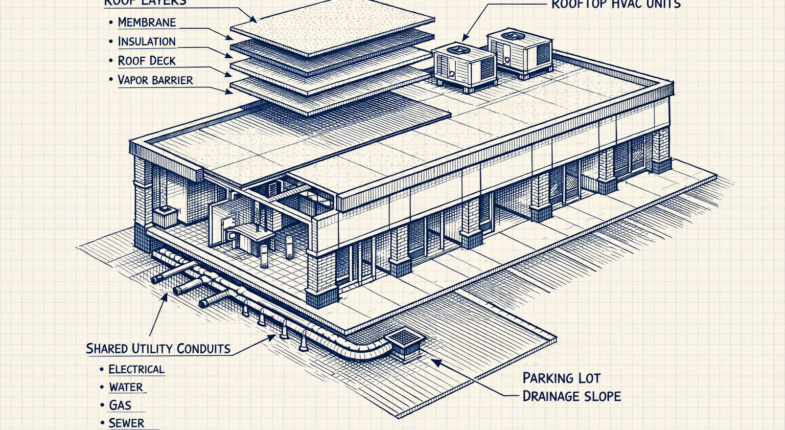

Deferred maintenance is another area where retail properties have their own set of problems. Flat roofs are standard on strip centers and they hold water and degrade in ways that aren’t visible from the parking lot. HVAC units are frequently shared across multiple suites or positioned on rooftops, which makes it easy for sellers to defer replacements for years. A parking lot that looks functional might still need restriping, drainage work, or full resurfacing to meet ADA requirements.

These aren’t cosmetic problems. They’re capital costs that hit faster after you take ownership. Staying ahead of these issues is one of the most underrated ways to protect your investment.

CAM reconciliation disputes are also worth your attention. Common area maintenance charges get estimated at the start of each year and then reconciled against actual costs. Smaller tenants in particular push back on reconciliation statements, and some leases cap CAM increases in ways that leave the landlord absorbing cost overruns. If a seller has unresolved CAM disputes from prior years, those can follow the property through a sale.

Experienced buyers go into due diligence with a checklist built from past mistakes. They review lease abstracts, not just rent rolls. They get roofing inspections and HVAC service records. They check if any co-tenancy thresholds are close to being triggered based on current occupancy.

First-time retail buyers focus on the income statement and miss the lease-level mechanics that can undermine it. The rent roll tells you what tenants are paying. The leases tell you under what conditions they get to stop. Knowing how to handle CAM disputes before they escalate is part of what separates experienced operators from first-time buyers.

Modeling a Value-Add Scenario Before You Submit an Offer

Once due diligence has shown you what’s broken, you can start to figure out what it’s worth to fix it. This is where underwriting changes from defensive to offensive - you’re no longer just looking for problems, but building a financial case for upside.

Start with what the property earns right now; it’s your current net operating income, calculated from actual rents minus operating costs. Then build a second version of that number - the stabilized NOI - market rents applied to every unit, including the vacant ones. The difference between those two figures is the value-add story in its simplest form.

But the gap only matters if you can close it at a cost that makes sense. To get from current to stabilized, you’ll probably need to spend money on tenant improvement allowances, carry vacant space through a lease-up period, and address any deferred maintenance found during due diligence. Those costs need to live in your model as line items, not rough estimates.

New retail construction in California usually runs between $261 and $413 per square foot. That number alone makes a strong case for repositioning existing retail instead of building from scratch. If you can buy a struggling strip mall, renovate it, and lease it up for a fraction of replacement cost, the economics can work in your favor - but only if you’ve priced the work.

The final piece is cap rate math. You’re buying at one cap rate and betting you’ll exit at another. If you buy at a 7 cap and stabilize the asset to trade at a 6 cap, that compression can add value on top of the NOI growth itself. Run scenarios and land on a price.

| Input | What It Represents |

|---|---|

| Current NOI | What the property actually earns today |

| Stabilized NOI | What it earns at full occupancy with market rents |

| CapEx to stabilize | TI allowances, lease-up carry, deferred maintenance |

| Entry cap rate | What you’re paying relative to current income |

| Exit cap rate | What the stabilized asset should trade at |

The honest question to ask yourself is whether the value-add story in the listing is real, or if it’s a seller repackaging a hard lease-up as an opportunity. Vacant space is only upside if tenants want to be there and the rent the seller is projecting is one the market will actually pay.

Running the Numbers Is How You Avoid Buying Someone Else’s Problem

If you’re actively searching, build your pro forma before you fall in love with a property - not after. Pull the rent roll, map the lease expirations, and pressure-test the cap rate against every vacancy scenario a seller can give you. That discipline won’t slow you down - it will save you from the deals that look clean on the surface and quietly aren’t.

The strip mall model still works in this market. But it works best for buyers who treat the numbers as the starting point - not the finish line.

FAQs

What cap rate range should I expect in San Diego?

San Diego strip mall cap rates generally fall between 5.0% and 6.5%, with coastal submarkets like La Jolla compressing toward the lower end and inland areas like El Cajon trading closer to 6.0%-6.5%.

How do anchor tenants affect strip mall valuation?

Anchor tenants create more predictable NOI and improve financing terms, often unlocking better loan-to-value ratios. However, if an anchor goes dark, co-tenancy clauses can allow smaller tenants to reduce rent or exit early.

What are co-tenancy clauses and why do they matter?

Co-tenancy clauses give tenants the right to reduce rent or terminate their lease if a named anchor vacates or occupancy drops below a set threshold. These provisions can significantly destabilize a rent roll after closing.

What due diligence items do buyers commonly overlook?

Buyers often miss co-tenancy clause triggers, deferred maintenance on flat roofs and HVAC systems, and unresolved CAM reconciliation disputes-none of which appear clearly on a standard rent roll.

How do I model a value-add strip mall opportunity?

Calculate current NOI, then build a stabilized NOI using market rents across all units. Subtract all capital costs-TI allowances, lease-up carry, deferred maintenance-and model the exit cap rate to determine if the upside is real.