San Diego’s Industrial Market in 2026: Vacancy, Rents, and What Investors Are Watching

June 22, 2026

Execution errors in 1031 exchanges are more common than most investors expect. The problem often isn’t ignorance of how a 1031 exchange works - it’s execution. A partial mortgage paydown created unexpected boot. The identification letter listed three properties but described one of them in a way that didn’t match the legal parcel. The timeline looked fine on a calendar but ignored a federal holiday that shifted the 45-day window by a day. These aren’t beginner mistakes - they’re the errors that experienced investors make because they assume the technical facts will sort themselves out.

Roughly 30% of attempted 1031 exchanges fail to achieve full tax deferral, and the failures don’t happen at the conceptual level. Investors who understand the exchange structure well enough to execute one are still tripped up by 1031 exchange boot calculation errors, identification rule technicalities, disqualified intermediaries, and - increasingly in California - misapplied reverse exchange strategies that introduce more danger than they resolve.

What follows is a direct look at where San Diego investors specifically are losing deferred gains - not through misunderstanding the law, but through the execution gaps that don’t show up until it’s too late to fix them.

Key Takeaways

- Roughly 30% of 1031 exchanges fail full tax deferral due to execution errors, not misunderstanding the law.

- Boot-taxable gains from cash differences or mortgage reductions-can trigger unexpected tax bills of 20-37% plus California state taxes.

- The 45-day identification deadline never shifts for weekends or federal holidays, and verbal communication doesn’t count.

- Identification letters must precisely describe replacement properties; vague language or incorrect parcel details can disqualify the entire exchange.

- Using a disqualified person as your Qualified Intermediary-family, recent attorney, or advisor-voids the exchange completely.

How Boot Gets Triggered Before San Diego Investors Realize It

Boot is the taxable portion of a 1031 exchange - the part the IRS treats as a capital gain even though you intended to defer everything - it shows up in two main ways and can happen without any obvious warning during the transaction.

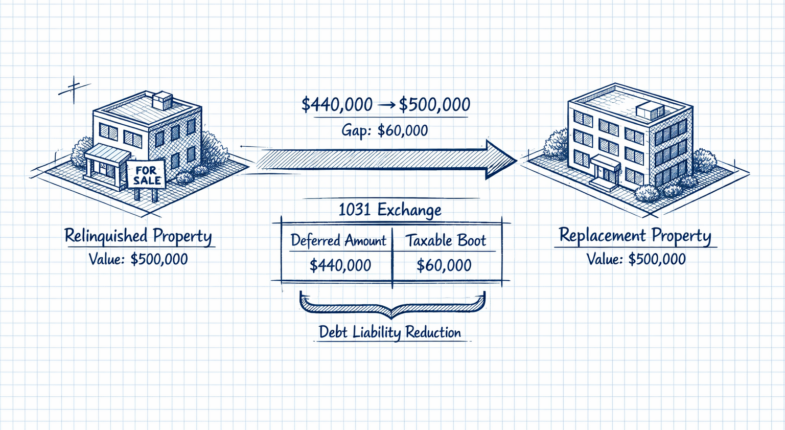

The easiest version is cash boot. If you sell a retail strip in Chula Vista for $700,000 and reinvest $640,000 into an industrial property in Kearny Mesa, that $60,000 difference doesn’t disappear - it can become taxable boot. To get full deferral, the replacement property needs to be equal to or greater in value compared to what you sold.

Mortgage boot is a little less intuitive but just as common. If your relinquished property carried $300,000 in debt and your replacement property only carries $200,000, the IRS treats that $100,000 reduction in liability as money you received. You can offset mortgage boot by putting in extra cash at closing. But it has to be planned ahead.

What makes this harder in San Diego is that the market tends to push investors toward properties with different financing structures. A seller moving out of a leveraged commercial building in Mission Valley might find that the replacement property in a different asset class carries far less debt by default. That debt reduction quietly gives you a taxable event.

The tax hit on boot is not small. Depending on your income bracket and how long you held the property, boot gets taxed anywhere from 20% to 37%. State taxes in California add even more on top of that.

Boot can also come from closing costs. If the exchange funds pay for non-qualifying costs - like loan fees or prepaid insurance - those amounts are treated as boot too. Your qualified intermediary should flag these in advance. But the responsibility to know them still falls on you as the investor.

The core issue is that partial reinvestment is a basic outcome to investors. Keeping a little cash from the sale, or trading down slightly in property value, seems manageable. But the IRS doesn’t grade on a curve - any amount not reinvested gets taxed and that number adds up faster than expected.

The 45-Day Identification Rule and Where San Diego Timelines Break Down

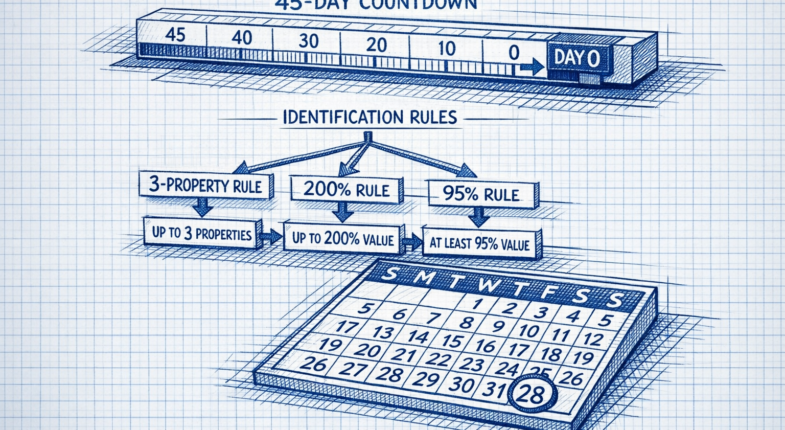

The IRS gives you 180 days to close on a replacement property after your relinquished property sells. But the clock that trips up most investors is the one that expires much sooner. You have 45 days from closing to find your replacement property in writing, and nothing about the San Diego market changes that.

That writing requirement matters more than most know. Your identification has to be a signed, written document delivered to a qualified intermediary or another permitted party before midnight on Day 45. A verbal conversation with your agent or a text to your intermediary does not count. No exceptions.

Here is where the calendar gives you a problem. If Day 45 lands on a Saturday, Sunday, or federal holiday, the deadline does not move to the next business day - it stays where it is. San Diego investors who assume the IRS follows standard business-day rules have lost exchanges over this.

The IRS gives you three ways to identify replacement properties. The first is the three-property rule, which lets you name up to three properties regardless of their value. The second is the 200% rule, which lets you name more than three properties as long as their combined value does not exceed double the value of what you sold. The third is the 95% rule, which lets you name any number of properties as long as you actually close on at least 95% of their total value.

Most San Diego investors default to the 200% rule when they should be using the three-property rule. If you sold a Kearny Mesa industrial property and want to find four replacement properties to keep your options open, the combined value of the four properties could push past the 200% cap and void your entire identification list. That is not a technicality to sort out later - it voids the exchange.

The three-property rule is simpler and harder to accidentally break - it does not matter what the properties are worth as long as you name three or fewer. For most San Diego transactions, that limit is workable and the rules around it are much less likely to be discovered at the last minute.

The right identification rule is closely tied to which properties you actually name. That is where the next layer of errors tends to appear.

Misidentifying Replacement Properties and What Disqualifies a Pick

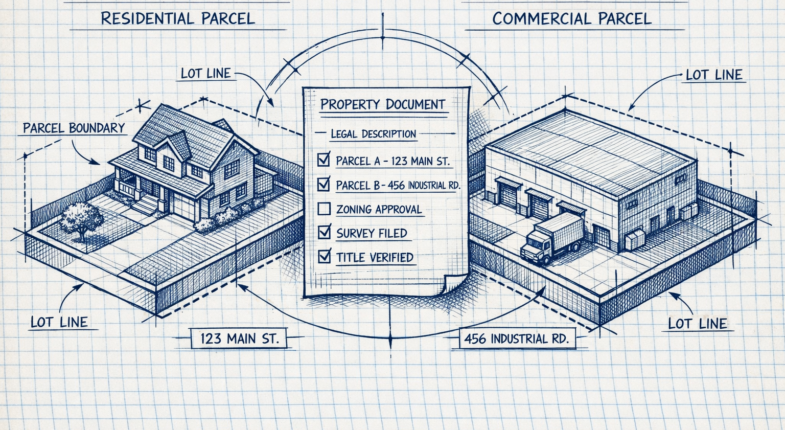

Once the 45-day clock is running, the identification letter you submit can become one of the most important documents in your exchange - it needs to describe each replacement property with enough detail that there’s no room for uncertainty. Treasury Regulation 1.1031(k)-1 sets out the standard and it basically says the description has to be enough to distinguish the property from any other property.

In practice, that means a street address is usually enough - but only if it’s the right street address for the right parcel. San Diego County has plenty of properties where a single address covers multiple parcels or where addresses are shared between adjacent lots. If you list the address of a commercial building in Chula Vista but the parcel number on record belongs to a neighboring lot, your identification could be considered invalid even though you were pointing at the right building.

The number of properties you list also matters. Most investors use the three-property rule, which lets you name up to three replacement properties without any restriction on their total value. If you list more than three, you move into a different rule set where the combined value of your identified properties can’t exceed 200% of the value you sold. Listing a fourth property without knowing about that puts your whole exchange at risk.

There is also a common misunderstanding about what “like-kind” actually means for property - it’s a wider concept than expected. You can swap a residential rental in San Diego for a commercial warehouse in Kearny Mesa. That still qualifies. What it does not mean is that anything goes. The property still has to be property held for investment or business use on both ends of the transaction. A personal residence does not qualify, and neither does property you’re looking to flip shortly after the exchange closes.

Commercial-to-commercial swaps within San Diego still need that like-kind confirmation in writing, and the identification letter is where it starts. Vague language like “a property near downtown” or “TBD warehouse in East County” will not hold up. The IRS expects you to name what you intend to buy, and anything short of that gives them a reason to disqualify the exchange before it ever reaches the closing table.

Choosing the Wrong Qualified Intermediary and Misusing Reverse Exchanges

Your Qualified Intermediary, or QI, is the person who holds your sale proceeds between transactions. The IRS has strict rules about who can fill that role, and the list of disqualified persons is longer than most investors expect.

Family members are not allowed to be your QI. Neither is an attorney who has represented you in the past two years, a financial advisor you have an existing relationship with, or an estate agent mixed up in the deal. These are called “disqualified persons” under Treasury regulations, and using one of them voids the exchange entirely - even if they do everything else correctly.

California does not currently license or regulate QIs at the state level, which means there’s no government body checking that yours is competent or financially stable. That matters because your funds sit with this person for as long as 180 days. You want to confirm they carry fidelity bonds and errors and omissions insurance, and that they hold exchange funds in a segregated account instead of a pooled one.

The other structural mistake worth covering here is the reverse exchange. A standard exchange sells first and buys second. But a reverse exchange lets you acquire the replacement property before your relinquished property sells. That is appealing to San Diego investors who worry about losing a property in a fast-moving market.

The structure works through an Exchange Accommodation Titleholder, or EAT. The EAT takes legal title to either the new property or the old one while you complete the sale side of the transaction. You still have 45 days to identify and 180 days to close everything, and those timelines run from the date the EAT takes title.

Reverse exchanges are more complex and expensive than forward exchanges, and they need experienced legal and tax counsel to structure correctly from the start. The terms of an EAT agreement can directly affect whether the IRS respects the exchange, so the depth of experience your advisors bring to that document matters.

The QI and the exchange structure are decisions you make before the process starts. Getting them wrong does not become visible until it’s too late to fix. Understanding the full commercial real estate underwriting process before you begin can help you avoid costly missteps down the line.

Filing Form 8824 and Keeping Your Exchange from Unraveling at Tax Time

For San Diego investors, the key mindset change is recognizing that a 1031 exchange is not a single transaction - it’s a sequence of interdependent steps where a mistake at any stage can eliminate the tax benefit entirely. A move from a Chula Vista rental to a Kearny Mesa commercial property is achievable, and investors make those kinds of moves successfully every year. But that success can depend on calculating boot exposure before the sale closes, picking a qualified intermediary with a verifiable track record, identifying replacement properties with language that holds up to scrutiny, and reporting everything to the IRS with the same accuracy that went into the deal itself.

If any part of that sequence feels uncertain - how to manage partial boot, how to structure an identification letter, or how to file Form 8824 accurately - the answer is to work with a tax professional and an estate attorney who specialize in 1031 exchanges in California before you list the property, not after you have already made a choice that can’t be undone.

FAQs

What is boot in a 1031 exchange?

Boot is the taxable portion of a 1031 exchange, triggered when you receive cash or reduce your mortgage liability. Even small differences in reinvestment amounts can create boot, which is taxed at 20-37% plus California state taxes.

Does the 45-day identification deadline shift for holidays?

No. The 45-day deadline never moves for weekends or federal holidays. If Day 45 falls on a Saturday or holiday, the deadline remains that day, not the next business day.

How must replacement properties be identified in writing?

Identification letters must describe each property with enough detail to distinguish it from any other, typically a precise street address matching the correct legal parcel. Vague descriptions like "warehouse in East County" will not satisfy IRS requirements.

Who is disqualified from serving as a Qualified Intermediary?

Family members, attorneys who represented you within the past two years, existing financial advisors, and agents involved in the deal are all disqualified. Using a disqualified person voids the entire exchange, even if executed correctly otherwise.

What is a reverse 1031 exchange and when is it risky?

A reverse exchange lets you acquire a replacement property before selling your relinquished property. It's more complex and expensive than a standard exchange, requiring an Exchange Accommodation Titleholder and experienced legal counsel to structure correctly.