Commercial Property Management Vista

March 17, 2026

How Commercial Properties Are Valued in California: Cap Rate, GRM, and What Sellers Often Miss

June 20, 2026

Most property owners and investors don’t find out they hired the wrong broker until something goes wrong. A listing sits too long. An offer falls apart during due diligence. A buyer walks because the pricing strategy wasn’t grounded in the latest submarket data - then you’ve lost time, momentum, and sometimes money. The problem isn’t obvious at the start - mediocre brokers can sound credible in a first meeting. Strong ones just perform differently when the deal gets hard.

What separates a high-performing commercial real estate agent in San Diego from an average one isn’t personality or pitch - it’s verifiable transaction history in your asset type, genuine submarket knowledge, access to off-market deal flow, and a close rate that holds up under scrutiny. These are things you can ask about directly, and things any broker should be able to answer without unnecessary delays.

This breaks down what to look for before signing a listing agreement or exclusive buyer representation agreement - and the questions worth asking to cut through the noise.

Key Takeaways

- San Diego operates as multiple distinct submarkets with different economic drivers, rewarding agents with deep local knowledge over generalists.

- Asset-type specialization matters more than firm size; verify what an agent has actually closed in your category within the last 24 months.

- Off-market access is critical, especially in slow markets-ask brokers how many of their last 10 deals were sourced off-market.

- Close rate, days on market, and fall-through rate reveal more about broker performance than active listing counts alone.

- Before signing, ask about exclusivity terms, dual representation, co-broking willingness, and how many deals they’re currently managing.

Why Commercial Real Estate in San Diego Operates Differently Than Most Markets

San Diego is not a single market - it’s a collection of very different submarkets that each run by their own laws, and that distinction matters quite a bit once you start talking to agents.

The metro GDP sits at around $257.3 billion and has grown roughly 15% over the last decade. That economic weight creates demand across asset classes. But it doesn’t spread evenly. Biotech and life science activity clusters in areas like Torrey Pines and Sorrento Valley. Military-adjacent industrial demand shapes corridors near bases that have nothing to do with general logistics patterns. Coastal retail answers to tourism and foot traffic patterns that inland retail doesn’t face. These aren’t just geographic differences - they’re fundamentally different economies layered on top of each other.

Then there’s the office market, which shows something different. The citywide office vacancy rate is sitting above 21%. That number points to a structural challenge - not just a slow quarter. Some submarkets are healthier than others. But the pressure is real, and it’s changing how office assets get priced, leased, and repositioned.

A generalist agent - or one who primarily works in residential and occasionally steps into commercial - tends to read these signals through too large a lens. They might apply general market optimism to a submarket that’s actually struggling, or miss the demand drivers that make an industrial corridor interesting. The difference between a surface-level read and an accurate one can translate directly into bad timing, wrong pricing, or a deal structure that doesn’t hold up.

San Diego also has some regulatory and zoning layers that add difficulty. Coastal Commission laws affect what can be built or redeveloped near the water. Land availability is constrained in ways that push development decisions into more difficult tradeoffs, often requiring careful thought around rezoning commercial property to residential. An agent who learned commercial real estate in a landlocked Sun Belt city won’t have that baked in.

None of this is meant to make the market sound impenetrable. San Diego is legitimately active and has opportunity across multiple asset types. But that opportunity is concentrated in ways that reward local knowledge - it’s why who you work with matters more here than it might in a more uniform market.

Why Asset-Type Specialization Should Be Your First Filter

Before you look at track record, personality, or firm size, start here. The type of commercial property a broker works with day-to-day shapes everything about how they work - their contacts, their read on pricing, and their sense of what a deal should look like.

A broker who closes industrial leases under 50,000 square feet is working in a market where vacancy sits around 4.6%. That means competition is fierce, available space moves fast, and knowing who holds the keys to an off-market property can be the difference between a signed lease and starting over. It’s a different world than a broker who lists vacant office space; the process means longer timelines, heavier concessions, and a much wider pool of available inventory.

These aren’t two versions of the same job. The strategies, the relationships, and the instincts are legitimately different.

A broker who claims to manage every asset type is spreading themselves thin. Industrial, retail, office, multifamily investment, medical - each one has its own set of players, its own rhythm, and its own ways that deals fall apart. Generalists can be helpful in certain contexts. But if you have a focused need, you want a person who has been in the room for deals like yours.

Find out what asset type the broker has actually closed in the last 24 months and how many transactions that covers. Not what they’re licensed for or what they’re willing to take on - what they’ve actually done, recently, in the category that matters to you.

If the answer is a combination of everything, that’s worth noting - it doesn’t automatically disqualify. But it should prompt a follow-up. Ask them to talk about a transaction in your asset type from start to finish. How they answer will tell you quite a bit about how deep their experience actually goes.

Specialization also connects to network. A broker who works industrial deals has relationships with landlords, developers, and tenants who are active in that space. That network is hard to build without staying active in one lane. For you as a client, that network is part of what you’re paying for. Understanding how negotiating commercial leases differs across asset types is one reason that specialized experience matters so much.

Get clear on asset type before anything else. Everything else you review will make more sense once you know the broker is operating in the right world.

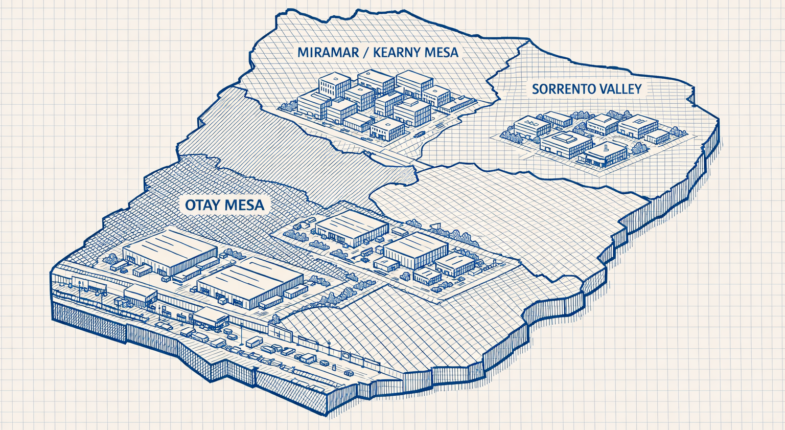

Submarket Knowledge That Goes Beyond ZIP Codes

San Diego is not one market- it’s a collection of tough neighborhoods that each behave differently and respond to different economic pressures. Sorrento Mesa draws life sciences and tech tenants. Kearny Mesa leans toward light industrial and flex space. UTC pulls in professional services and financial firms. Downtown operates under its own set of laws around density and mixed-use development. Chula Vista is a different conversation altogether as it attracts logistics users and benefits from its proximity to the border.

A commercial estate agent knows these distinctions without having to look them up. They can tell you which corridors are quietly tightening and which ones have more availability than the headline numbers let on.

This matters in a helpful way. City-wide vacancy rates and average asking rents are easy to find. But they smooth over detail. A submarket that looks balanced on paper may have a very thin supply of the space you want in the size range you need. An agent with geographic depth will flag that without you having to ask.

It’s worth pressing your agent on this. Ask them about absorption patterns in the neighborhoods you’re thinking about - not just if space is available, but if demand is growing, holding steady, or starting to pull back. Ask them which tenant types are expanding in that area and which ones are quietly consolidating. If they can answer that without a pause, you’re in good hands.

Submarket knowledge also shows up in pricing. Lease rates on paper don’t always tell the full story because landlord concessions, tenant improvement allowances, and free rent periods can vary quite a bit by neighborhood and building class. An agent who works a submarket closely will know where landlords are negotiating and where they’re holding firm.

The difference between an agent who knows San Diego and one who knows your target submarket is the difference between general advice and usable intelligence. You want a person who can tell you what a basic deal looks like in a specific submarket - not just what the wider North City numbers say.

Geographic depth is something you can test in the first conversation. Ask your agent to talk about what’s going on in two or three neighborhoods. The quality of that answer will tell you quite a bit about how helpful they’ll be when it counts.

Off-Market Access and Broker Networks That Actually Move Deals

What gets listed publicly is only part of what’s available in San Diego’s commercial market. A broker with deep local relationships will know about properties and motivated sellers well before anything hits a listing platform - and in a slow-absorption environment, that head start matters quite a bit.

Consider the office market as a reference point. In 2024, only 29 office transactions closed across San Diego for a combined $703.7 million; it’s a thin slice of activity spread across the whole year. When deal volume is that low, waiting for publicly listed inventory to find you is not a great strategy.

The brokers who move deals in conditions like that are usually the ones with a network - investors, owners, developers and other brokers they’ve built trust with over time. Those relationships surface opportunities that never get listed because the seller doesn’t need to cast a wide net. They already have a call out to people they trust.

That’s especially worth thinking about if you’re trying to sell commercial property in San Diego. An experienced broker with off-market connections can put your property in front of qualified buyers directly, instead of waiting for the right buyer to stumble across a listing - and that’s a meaningful difference when absorption is slow.

It also works in reverse for buyers. Off-market deals tend to have less competition and more room to negotiate because you’re not up against a field of other bidders responding to the same public listing. Fewer parties at the table changes the outcome.

To know if a broker has this access, ask them. A helpful question to put to any broker you’re looking at is how many of their last 10 deals were off-market. Their answer tells you quite a bit. A broker who closes deals through their network will be able to name specifics. One who relies mostly on public listings will have a harder time answering.

You can also ask how they stay in touch with other brokers in the market. Co-brokerage relationships matter here as well. A broker who other brokers want to work with will hear about more deals. That network takes years to build and can’t be faked.

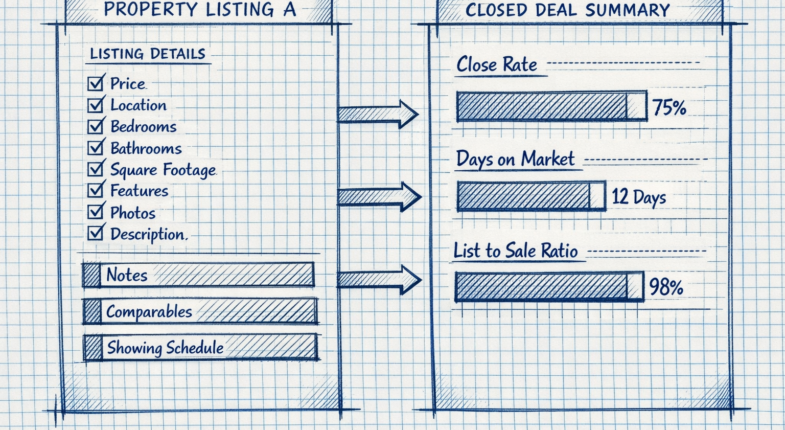

How to Actually Evaluate a Broker’s Close Rate (Not Just Their Listings)

A long list of active listings looks great but doesn’t tell you much. What you want to know is how many of the deals closed - and on what terms.

San Diego’s commercial leasing market has pulled back hard. Activity dropped around 35% year-over-year to roughly 1 million square feet, which is a 15-year low. In a slower market, the difference between brokers who list and brokers who close gets much wider; it’s why close rate deserves more of your attention than a portfolio of signs on buildings.

When you sit down with a broker, ask them for their close rate. A strong broker should be able to give you a number and explain the context behind it. If they pause or redirect to how many listings they have, that tells you something too.

Beyond close rate, there are a few other numbers worth asking about. Average days on market is one - it shows how long their listings usually sit before a deal gets done. You also want to know their list-to-sale price ratio, which compares what a property was listed for to what it sold or leased for. A pattern of large gaps between those two numbers can point to overpricing or weak negotiation.

Fall-through rate is another one to bring up - the percentage of deals that go under contract but never make it to close. Some fall-throughs are unavoidable. But a high rate can mean deals are being poorly structured from the start. A broker who tracks this number and can speak to it is a broker who pays attention to the full process.

It’s worth asking for this data in writing if you can. Transaction history, closed deal summaries, or an easy spreadsheet of recent closings all give you something concrete to review. Testimonials are fine but they don’t replace performance data.

Brokers who give you clean closing data - not just activity - know their own track record well enough to stand behind it. That level of transparency is a sign that they’ll bring the same attention to your deal. If you’re not sure where to start, learning how to evaluate any real estate professional by the numbers is a skill that pays off every time.

Questions to Ask Before Signing a Listing Agreement or Buyer Rep Agreement

Once you’ve done your homework on a broker, the last step before committing is a direct conversation. These are the questions worth asking out loud - not just thinking about.

Start with exclusivity. Ask the broker to talk about what the agreement actually locks you into. Some listing agreements are exclusive for 12 months with no easy exit, so you want to know what happens if things aren’t moving after 90 days.

Ask how they plan to market the property or find you a deal. A broker should be able to describe their strategy and explain it - not just say “we’ll push it to our network.” You want to hear specifics about how they get in front of buyers or landlords past the MLS.

Find out how many active deals they’re working right now; it’s a fair question. A broker juggling 20 transactions at once might not have the bandwidth to handle yours the way you’d want.

Ask directly about co-broking. Some brokers are reluctant to share commission with a buyer’s rep. That can quietly limit how many people see your listing. You deserve a straight answer on this before you sign anything.

Dual representation is worth raising too. Ask them: if they find a buyer through their own network, do they represent both sides? Some brokers will, and that’s a conflict of interest you should know about going in instead of discovering later.

One question to not skip: ask what they need from you for them to do their job well. A broker who can answer this has probably done it before. One who looks taken aback might not have a process.

Finally, ask how they communicate and how often. Do they send weekly updates? Do they call or email? The frustration of not hearing back mid-deal is real, and it’s worth setting expectations.

None of these questions are confrontational. They’re the kind of thing any seasoned broker expects to hear from a person who takes their investment seriously. If a broker bristles at them, that tells you something helpful before you’ve signed a single page.

Picking the Right Broker Is the First Deal You Make in San Diego CRE

Hiring a commercial real estate agent is a transaction - one that deserves the same scrutiny, the same due diligence, and the same willingness to walk away if something doesn’t add up. The questions you ask before signing a representation agreement are just as important as the ones you’ll ask at the negotiating table.

Take your time with this choice. The right agent will welcome the hard questions - and their answers will tell you everything you need to know.

FAQs

What should I look for in a San Diego commercial real estate agent?

Prioritize verifiable transaction history in your specific asset type, genuine submarket knowledge, off-market deal access, and a strong close rate. These are measurable qualities you can ask about directly before signing any agreement.

Why does asset-type specialization matter when choosing a broker?

Each commercial asset type-industrial, office, retail, medical-has its own pricing dynamics, relationships, and deal structures. A broker who specializes in your asset type will have deeper contacts and more relevant experience than a generalist.

How important is off-market access in San Diego's commercial market?

It's critical, especially in slow markets. With only 29 office transactions closing in 2024, waiting for public listings is a weak strategy. Ask brokers how many of their last 10 deals were sourced off-market.

What metrics best reveal a commercial broker's true performance?

Focus on close rate, average days on market, list-to-sale price ratio, and fall-through rate. These numbers reveal far more about a broker's effectiveness than how many active listings they currently hold.

What should I ask before signing a listing or buyer rep agreement?

Ask about exclusivity terms, their specific marketing strategy, how many deals they're currently managing, co-broking willingness, dual representation policies, and how often they communicate with clients throughout a transaction.